July 2022 - Up, up, and away!

July has proven a remarkable recovery - My portfolio is up big and I had some time to enjoy the summer holiday and celebrate turning 29. Big news for Unity, earnings out for my biggest holdings, and a few other things.

Changes to my portfolio this month

July was a quiet month in terms of purchasing shares, but a lot more interesting when it comes to performance.

Growth Portfolio

Overview

Unlabeled on the chart from left to right: Alphabet (1.4%), Xiaomi (1.0%) & Coinbase (0.1%)

Moves

On July 15th Alphabet (GOOGL) issued a stock split of 20-to-1.

Performance

My Growth Portfolio saw tremendous returns this month of 24.34% outpacing the market significantly.

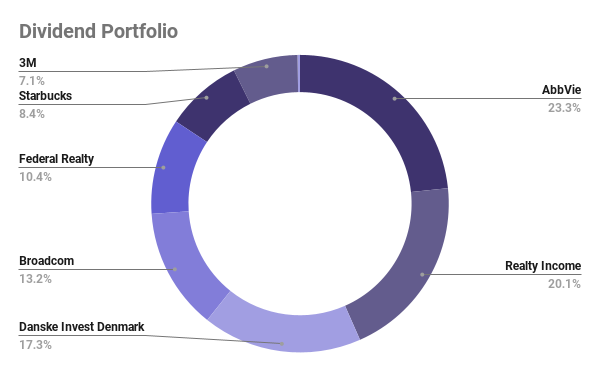

Dividend Portfolio

Overview

Unlabeled on the Chart: Orion Office REIT (0.3%)

Moves

A small automatic buy order of the Danish Invest Denmark Index ETF went through on the 8th - Which I aim to continue doing every month this year.

Performance

My Dividend Portfolio returned 6.48% in July. While admirable this trailed the market by nearly 4%.

Dividend overview

| Name (Ticker) | Received | Amount (USD) |

| Broadcom (AVGO) | Jul 1st | $20.05 |

| Nvidia (NVDA) | Jul 4th | $0.78 |

| Taiwan Semiconductor Manufacturing Company (TSM) | Jul 15th | $38.31 |

| Federal Realty Investment Trust (FRT) | Jul 18th | $21.57 |

| Orion Office REIT (ONL) | Jul 18th | $0.50 |

| Realty Income (O) | Jul 18th | $13.72 |

| Comparison YoY | $64.37 (Jun 2021) | $94.93 (+$30.56) |

Dividends received before taxes. Comparison to the same month a year prior.

Commentary & Review

This month has been very good to investors, in particular in its latter half when Q2 earnings started rolling out. My biggest holding, Tesla (TSLA) kicked off the party with an impressive performance considering headwinds against them this quarter. While there was no getting around the fact that their Shanghai factory was shut down for three weeks doing Covid lockdowns in China, the company still managed to grow 42% YoY. Solar production finally bumped up a little, their two new factories are ramping fast and on schedule and June became the best single month ever in terms of production. They also managed to get rid of most of their Bitcoin (BTC) holdings at pretty much break-even, marking an impairment of their remaining holdings equivalent to the profit they have taken. The stock has recovered greatly from bottoming out in June at below $700, sitting now at nearly $900 per share. Microsoft (MSFT) & Alphabet (GOOGL) managed to miss on earnings ever so slightly, with a massively positive reaction from a market expecting much worse. Microsoft has also been picked by Netflix (NFLX) to become its global advertising partner, which could be very exciting.

In anticipation of Alphabet's earnings, I made a post of five things to consider about the stock. It became the newest addition to my Growth Portfolio just a few months ago, and it remains an extremely popular stock pick right now. Given that it is trading at a decade-low P/E and the company's size and reputation, I wanted to give some insights into what I look at beyond the numbers. On July 28th the Fed hiked interest rates by another .75 basis points, indicating a willingness to get control over record high inflation - which again the markets seemed to like. Amazon (AMZN) topped it all off with their earnings report showing improved Q3 guidance and a beat on revenue. The stock went up more than 10% on the last day of trading in July, which also helped move my Growth Portfolio back into the green for the trailing last 3 months. The portfolio is still down 10.3% YTD but considering I was down more than three times this (33%) of this just 2 months ago, I am very much satisfied. The Dividend portfolio continues its solid, much less volatile performance and is now green YTD, up 2.22%, doing much better than the market overall.

Finally, I believe it is worth mentioning that the big concerning issue with 3M (MMM) which has made me hesitant to add more shares, now finally seems to be easing. Following their earnings, the company announced they are filing for Chapter 11 (partial bankruptcy) in the business unit responsible for a massive amount of lawsuits related to alleged faulty earplugs for the military. The business called 'Aearo' was a company acquired by 3M back in 2007, long before I became an investor. It is ultimately the best way to deal with a really unfortunate situation: A fund of $1 billion has now been set aside for veterans suffering from hearing loss as a consequence of Aeros failures and should now be able to receive compensation much faster rather than pursuing individual litigation. It also means the problem is now mostly contained and that 3M can continue to operate without having to worry too much about this issue, which could, if left unchecked, have ended up costing trillions (much more than the entire company is worth today).

3M has a product portfolio of over 60.000 different products. They invented and produce many of the things we use every day. Ultimately the 'Aeros' business is a very small part of a big puzzle.

I am glad to see this and have been eagerly waiting for some kind of resolution. The stock also reacted positively to the news, though I remain slightly down on my position. They seem now to be streamlining the business a little also announcing plans to spin off their healthcare business unit. 3M may not be the most exciting company in the world, but they have proven time and again to be resilient. The company pays a dividend above 4% and has increased its payouts without pause for more than half a century.

Dividends

July has likewise been a great month for dividends. Compared to July last year my dividend income has grown nearly 50%. This is largely due to opening a position in Broadcom (AVGO) which I did not own back then. However, Realty Income (O) and Taiwan Semiconductor (TSM) have both increased their yields as well. If I can manage I would like to add another dividend-yielding asset to my portfolio this year (whether it be an existing position or not), but regardless I still plan to keep growing my dividends consistently - and it may end up a much larger focus for me, as a market downturn truly has shown me the power of this approach.

Research & Goals

Earlier in the month prior to earnings, on July 13th Unity (U) announced a big change: They are merging with app monetization provider ironSource (IS). ironSource is an Israeli-based company, employing just around 1000 people trading at a market cap prior to the deal of around $2.6 billion. Despite being called a merger, this is in reality more of acquisition by Unity, as they are a much larger company by valuation and size. However, unlike Unity, ironSource is already profitable, which is really good news. The deal has sparked much attention and controversy as it is an all-stock deal of originally 4.4B representing a premium of 74%. This is quite massive and will result in share dilution of 29% - which Unity plans to counter in a rather odd way of initiating a soon-to-come share buyback program of $1 billion and raising this capital through their two largest institutional investors. Here are my initial thoughts, however which I posted to Twitter:

The situation is complex and this is a huge deal for the company. More concerning to me, however, has been the developer community's response to the deal, deeming ironSource an adware company and the deal as a sign of Unity moving in the wrong direction. I have spent most of my time this month researching the topic and have a lot more thoughts to share in a dedicated post once I hear more from Unity in their upcoming Q2 earnings report. I expect growing pains from this and the reaction to the deal has revealed lackluster communication efforts from the company, but overall as mentioned in my tweet, it seems to fit with my long-term case and may actually have been a really good value for Unity to snap up a competitor/partner beaten down by the bear markets.

Speaking of bear markets, for some time now, the goal I set out for my portfolio to return 35% this year has seemed ridiculous. Just last month I was in the red by 27%. Now it is only 10% and I continue to strive toward this goal. 1 year is not long-term, but all the noise of the last few months have only helped me gain perspective. Among others in my portfolio, I strongly believe both Unity and Tesla are trading at far below what is justified and expect a jump here before the year has ended.

Watch List

Growth Portfolio

| Name (Ticker) | Conviction (Rank) |

| Embracer (EMBRAC B) | 1 --- |

| Sea (SE) | 2 --- |

| Meta (META) | 3 ↑ |

| Shopify (SHOP) | 4 ↓ |

| Palantir (PLTR) | 5 ↑ |

| MercadoLibre (MELI) | Contender |

Note that many of these may already trade within desirable price ranges for me but may overlap with current holdings with higher conviction or are simply on hold due to a lack of funds.

Dividend Portfolio

| Name (Ticker) | Conviction (Rank) |

| Bank of Nova Scotia (BNS) | 1 ↑ |

| JP Morgan (JPM) | 2 ↓ |

| Costco (COST) | 3 ↓ |

| Digital Realty (DLR) | 4 --- |

| Lockheed Martin (LMT) | 5 --- |

| Corning (GLW) | Contender |

Note that many of these may already trade within desirable price ranges for me but may overlap with current holdings with higher conviction or are simply on hold due to a lack of funds.

There has been slight movement in my Watch List this month. Despite Meta (META) delivering a lackluster earnings report, I cannot stop thinking about just how interesting their situation is; To me, they are now essentially a value stock - trading at a low P/E with little to no growth in the short term, but at the same time they are making one of history's investment bets. Their bet on the Metaverse is exciting to me and I fully agree that it may change our lives. The odd thing is, no one knows how it may take shape. Zuckerberg recently alluded to Meta being in 'deep philosophical competition with Apple" who are allegedly also on the way with something incredibly exciting in the XR space. Most of the growth companies on my Watch List are now more a question of entering at the right time, than if - with the exception of Shopify (SHOP) and MercadoLibre (MELI) which I both moved down the list because of a bigger lack of faith in their operations.

For the Dividend Portfolio Watch List, Bank of Nova Scotia (BNS) has taken the top spot in place of JP Morgan (JPM). I am nearly certain now that my next position for the Dividend Portfolio will be in Finance, I just like the idea of owning a non-American bank slightly better than the other. JP Morgan has also announced suspending their buyback program, which I do not quite understand as they are trading at very low levels.

Goals

Short term I wish to continue to increase my position in Unity - potentially Coinbase and Xiaomi as well.

For the year 2022, I prioritize buying growth over dividend stocks.

I have no plans to open new positions in my Growth Portfolio.

I do not plan on selling out of any more positions this year.

In my 2021 year in review, I stated that I aim for a 35% return in 2022. I continue to strive toward this goal although I have accepted its unlikeliness. Currently, I am down 10.3%.

Over the long term, my goal is to slowly shift towards more stable positions and dividends on my journey towards financial freedom.

Disclaimer: I am not a financial advisor, the opinions expressed in this article are entirely my own – always invest at your own risk.